By Tefo Mohapi

Hailed as the “Kenyan technology success story,” many have claimed M-PESA to be a testimony to the greatness of the East African country’s technology scene, producing world-class technology companies that rival those in South Africa. However, is the acclaimed mobile money service really Kenyan at all?

The answer is no, M-PESA is British.

By any stretch of the currently available facts, the service that accounts for more than 60 percent of Kenya’s GDP in transactions was conceived by British professionals. The company commissioned with developing the idea, Sagentia, into a workable technology was British. Additionally, the company that owns the intellectual property rights to the idea, Vodafone, is British, and, lastly, it was funded in its initial stages by the British Government.

Initial stages of a mobile money system

The story, according to Paul Makin, former M-PESA architect and professional in the UK banking sector, started before 2007. Makin says that the “original team was Nick Hughes and me. I came up with concept and architecture.”

On the question of why they settled on the name M-PESA, perhaps the only Kenyan aspect of the innovation, Makin said: “We talked as a team in a Nairobi bar. Came up with it, asked the batman (sic). He liked it, so it stuck.”

“Nick forced it through the business (UK’s Vodafone). Susie Lonie joined after about 6 months.”

All this took place in 2004 before the service was to be launched in Kenya 3 years later in 2007 through Safaricom Ltd, a Vodafone majority-owned telecommunications company in Kenya.

It is during these initial stages, pre-launch in 2007, that Hughes pitched the concept to the “powers that be” at Vodafone in the UK. Vodafone quickly realized the potential in the concept and decided to match the £1 million funding provided by the British Government’s Department for International Development to further develop the concept.

With funding secured, it was time to turn the concept into a working service and test it.

Sagentia, a British technology development company with headquarters in Cambridge, tendered to develop the concept and was selected as the technology partner to oversee the development of the user application which would sit on the mobile phone, the communications software sitting within the network (Vodafone, Safaricom), and the centrally hosted account management system.

According to Makin, the decision to go with Sagentia was a decision agreed to by the whole team.

Even during these stages, there is a hint from Makin that the concept received some resistance from within Vodafone, with them wanting to “pull the plug” at a certain point, but with the significant help of Michael Joseph, former CEO of Safaricom and now Vodafone’s Director of Mobile Payments, the concept came to be accepted within Vodafone.

On how big an impact Joseph had on the success of M-PESA, Makin says: “A big one. Wouldn't have happened without him. He made sure SF (Safaricom) worked with us and worked with Nick to get it through VF (Vodafone).”

Sagentia further worked with Vodafone throughout the development phase of both the pilots and the full rollout. An extensive market needs analysis for potential users and stakeholders and extensive prototyping was run so that the service and user interface would be accepted.

During March/April 2007, Vodafone launched M-PESA in Kenya, and the rest, as they say, is history.

A Kenyan innovation

Makin insists that M-PESA is a Kenyan innovation. He explains: “There were the agents, who worked very hard. Without agents, M-PESA is nothing.”

Unfortunately, whether technology is of a certain country cannot be determined by the “agents” who were involved in pilots, roll-out, or as “resellers”.

On the question of why they settled on the name M-PESA, perhaps the only Kenyan aspect of the innovation, Makin said: “We talked as a team in a Nairobi bar. Came up with it, asked the batman (sic). He liked it, so it stuck.”

Many technology companies that are European or American have agents and resellers in each country they operate in and as such, this does not instantly mean they are now Kenyan, Nigerian, or South African. This part of Makin’s argument that M-PESA had Kenyan involvement in its innovation or development stages is not convincing.

There is, however, an interesting twist in the tale.

Could the “real” M-PESA innovator please stand up?

Nyagaka Anyona Ouko, a Kenyan from Nairobi, claims he is the innovator of M-PESA and claims that Vodafone and its representatives stole the idea of Mobile Cash Transfer from him.

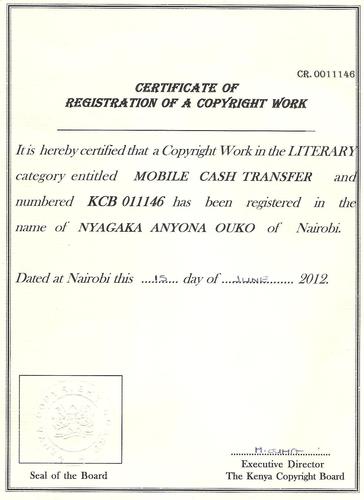

Ouko presented me with a certificate from The Kenya Copyright Board dated 15 June 2012 which reads:

“It is hereby certified that a Copyright Work in the LITERARY category entitled MOBILE CASH TRANSFER and numbered KCB 011146 has been registered in the name of NYAGAKA ANYONA OUKO of Nairobi.”

Despite this certificate being awarded in 2012 and being stated as being in the LITERARY category, Ouko insists he is the original M-PESA innovator and further elaborates by saying that he has been “trying to Patent a Money Transfer system way back in 2003”.

Even though he says that he believes many more Kenyans contributed to the innovation and development of M-PESA without recognition or reward, he writes, “Even though I currently believe I am the one, I start this with an open mind. If another person or firm comes forward with compelling proof I am ready to step aside and support that person.”

He adds: “By 2003 I was running a simple M-PESA system and earning money!”

Ouko claims that he presented Safaricom with a “concept document” and alleges on his blog that “If you see the document I sent to @SafaricomLtd you will understand that. All they did was code!”

Mobile Money Transfer Service

Since the launch of the Vodafone Mobile Money Transfer Service, popularly known as M-PESA, in Kenya five years ago, Safaricom has faced a wave of allegations claiming the telecoms giant ‘stole’ the idea. One unresolved case has even ended up in the courts.

Another case, although not in court, stands out because the accuser, Nyagaka Anyona Ouko, has produced proof of a copyright certificate leaving the legal fraternity scratching their heads and others raising questions.

His claim to being the “M-Pesa Innovator” becomes more curious as we learn (as per half-year results released by Safaricom in 2012) that Safaricom pays a “license fee” to Vodafone in the UK for their use of M-PESA in Kenya. This raises questions of whether Safaricom or Vodafone holds any copyrights or patents whatsoever in Kenya for mobile money transfer.

M-PESA was launched in April 2007.

Before we get ahead of ourselves, let us tell Ouko’s story from his early days.

Driven by necessity

The story starts in 2002 when Ouko wanted to send money to his ailing mother in a remote village. Ouko faced limited methods of transferring the money and takes up the story:

The only legal way of sending money by then was through the use of Money Order or Express Money Order which were being offered by the Postal Corporation of Kenya. However, those methods required that my mother had to travel some distance to pick up the money. I also had to find time and travel to the local post office where I could do the transaction.”

“The most popular way of sending money than was by bus. However one had to hang around the bus station for buses plying the upcountry routes. I come from Gesusu village and by then Kisii District, currently Kisii County. So I could hang around and on a good day find a fellow villager whom I could entrust with the money. On some occasions of course the money never got home.”

With this need in mind, Ouko had a “Eureka” moment and realized:

“If I send my mother some airtime, she could probably convert it to money somehow. This is because I had on occasions sent airtime before. This I could do by scratching the number and reading it to the person at the end of the line. The person could jot it down and then load it later.”

So he went on to arrange with a shopkeeper friend of his in his mother’s village that he send him some airtime then he in return gives my mother some cash. The shopkeeper agreed and only charged him a 10 % “administration” fee.

Countrywide expansion

With the agreement with the shopkeeper in his mother’s village working smoothly, Ouko set out and started planning to roll out a similar method of money transfer across Kenya. The plan as he retells his story was to have an agent in every town.

“The movement of the money was to be SMS based. The only security in the system by then was the number from which the message was coming. So long as the agent knew the number used to send the message he went ahead and paid the money.” he said.

Ouko then went ahead and started setting up agents across various towns in Kenya, starting with Kisii, Kisumu, Nakuru, and Nairobi. He, unfortunately, faced some hurdles in these early stages.

“However before the business could take off I discovered I needed a bank account. This is because the agents required a medium through which they would transfer the money faster. Just to be sure the agents don’t lack money when they are paying out. The plan initially was to ensure the agents had cash for the transactions. The only medium which was moving was the message. Then the balancing of books would be done at the end of the month,” he elaborated.

As if this hurdle was not enough, the whole business almost came to a crashing end when Ouko experienced even more obstacles.

Startup obstacles

Startups in Afrika face many obstacles ranging from lack of funds for starting up and expansion, up to and more frustratingly including government red-tape and bureaucracy. Ouko experienced one such frustrating experience which forced him to change strategy and led him into more obstacles.

Needing to open a bank account to better run the business, he headed to Kenya’s Attorney General’s office to register the business name, MOBICASH MONEY TRANSFER Ltd. This is required by law in Kenya that before opening a business bank account one should have registered a business name with the Attorney General’s office.

Dead-end

At the Attorney General’s office all seemed well when a search was done and the name was found to be available for registration, but, just before he could get the registration Ouko was informed that “they required a letter from the Ministry of Finance – Treasury clearing me to run a money related business.” as he retells his visit.

So, as instructed, he headed to the treasury office where more bad news awaited him, more like a dead-end to his continuing his mobile money transfer business.

Ouko says of his visit to the treasury “The lady told me that first and foremost I was in an actual sense running a briefcase bank. She asked me to tell her that I was willing to stop that business with immediate effect. Failure to which she would send in the police. She also told me that before I could be advised of the requirements I needed to prove that I had in my bank account (I did not own a bank account back then save for a Postbank one) Kshs 10 million. Actually she even went ahead to advise me that once I had the money in my account then I will come back and be allowed to see her in her office.”

This proved to be the final blow to Ouko running his mobile money transfer business independently, he would have to re-strategise because as he narrates his story, he didn’t have Ksh 10 million and didn’t know where to raise Ksh 10 million.

Mentor and detour

With that blow being dealt with his dream to run the business independently and many naysayers telling him it’s not possible, Ouko garnered more strength amidst the negativity. He also sought advice from many people as he retells, but one such notable person is Mtumishi Augustino Njeru Kathangu.

Kathangu, or Mtumishi as he is popularly known, is a former member of parliament in Kenya. He is currently the Secretary-General of the “Forum for the Restoration of Democracy-Asili” (FORD-Asili) among many of the organizations he is involved in.

Ouko was introduced to Kathangu by his longtime business partner, Patrick Musembi. Believing that Kathangu’s political connections, experience, and knowledge could possibly assist him in setting up his mobile money transfer business.

As Ouko narrates “Therefore one afternoon, in September 2003 armed with a note from Patrick Musembi to introduce me, I met Mtumishi. We had a long chat whereupon I explained to him what proposal I had which I wanted to deliver to specifically Safaricom. He asked me why I was only thinking about Safaricom, I told him because I believed that Safaricom was above board and I would be very comfortable dealing with them. He actually went ahead and gave me a short lecture about Safaricom.”

A lecture, it turns out, that Ouko has asked that we not retell. He does say though that Kathangu warned him that any idea or concept he has, he should assume it will not be safe with anyone or any company.

“He actually advised me to try and seek some form of IP protection. To be honest. He was the first person to tell me point blank that not all good those nice-sounding companies will care about protecting my idea. He actually painted a picture of very hungry companies which will not hesitate to even gobble one whole if it meant adding some more profit. At the time it was very difficult to understand and believe but I got the message.” Ouko said.

Armed with that advice from his newly found mentor, Ouko wrote his first proposal and delivered it to the Kenya Industrial Property Institute (KIPI) in December 2003. This trip, marked the start of a detour in Ouko’s business strategy as his pursuit to run it independently failed.

Ouko continues and tells of his visit to KIPI “whereupon I briefly talked to a gentleman who explained to me that KIPI only gave protection to utility models. He flipped through my booklet and advised me that the document will be better protected by the Kenya copyright office (KECOBO).”

Missing documents

Being the businessman he is, Ouko in 2004 started an aviation college in Dar Es Salaam, Tanzania with the assistance of investors, but before departing for Tanzania he dropped off his proposal at the KECOBO where he was instructed to check back within a month.

“I left for Tanzania and the ensuing months I was always on the move. . I went back again in April 2005. The guys I found did not know about the document I had deposited with them so they again asked me to deposit with them yet another one. “ Ouko says.

As if that wasn’t enough, Ouko retells another missing document “Come November 2005 that too was missing. So I requested the services of a Lawyer Mr. James Ong’ondo. When I came back in April 2006 he already had a letter from the copyright board. So now I was happy I was protected.”

“Armed with a copy of the copyright letter, a cover letter, and a copy of the proposal the lawyer deposited the documents at the offices of the then Managing Director Michael Joseph. I still have the signed delivery book up to this day.” Ouko adds.

Having delivered his Mobile Cash Transfer proposal to Safaricom Ltd’s then Chief Executive Officer, Michael Joseph, Nyagaka Anyona Ouko was told to wait a few months as the company looked into it. It turned out that the only other time he would “hear” from the company again was when they launched M-PESA in 2007, on Kenya's Citizen TV.

As reported in Part II of this series, "The curious case of Nyagaka Anyona Ouko, the mobile money transfer innovator - Part II, Ouko felt his best option at developing his mobile cash transfer business was in partnership with Safaricom. When in April 2007 he saw the company was launching a similar service called M-PESA, he lost all hope and believed they had “stolen” his idea.

Safaricom disagree. Speaking to me, Nzioka Waita, Director of Corporate Affairs at the telecommunications services provider, said this is a good opportunity and platform for the company “to put to rest some of the misconceptions that have existed within the tech community.”

Is M-PESA really Kenyan or British?

In introducing this series, the initial question was "Is M-PESA really Kenyan or British?". In addressing this question, Waita explains that it is neither Kenyan nor British.

Waita said that “M-PESA as a mobile money transfer platform is the product of years of collaborative research and innovation-driven by teams in Kenya, the UK and other parts of the world. As to who owns the intellectual property rights in M-PESA, that is also quite simple, the IP is in two forms, i.e. the trade mark and the proprietary software design and functionality. The IP in the trade mark M-PESA is jointly owned by Vodafone and Safaricom in Kenya, while Vodafone owns the trademark outside Kenya. The IP in the technology (read patents) is owned by Vodafone.”

Having said that, the assertion and conclusion that M-Pesa is British were made after looking at the parties involved in its development and funding.

“The article [you are writing] is not entirely inaccurate in terms of the history of the development of M-PESA to the extent of the involvement of Vodafone, DFID, and others. However, the story fails to mention that the product/service for which VF (Vodafone) was granted funding was actually a microfinance repayment solution. It was piloted in Thika, Kenya by Safaricom and Faulu Kenya. During the pilot, Safaricom realized that people would use the system to transfer money and not to repay their loans as they had the menu on their phones. At this juncture, Vodafone commissioned Sagentia to re-write the software as a mobile money transfer solution.“ Waita added.

Unsolicited proposal and weighty priority

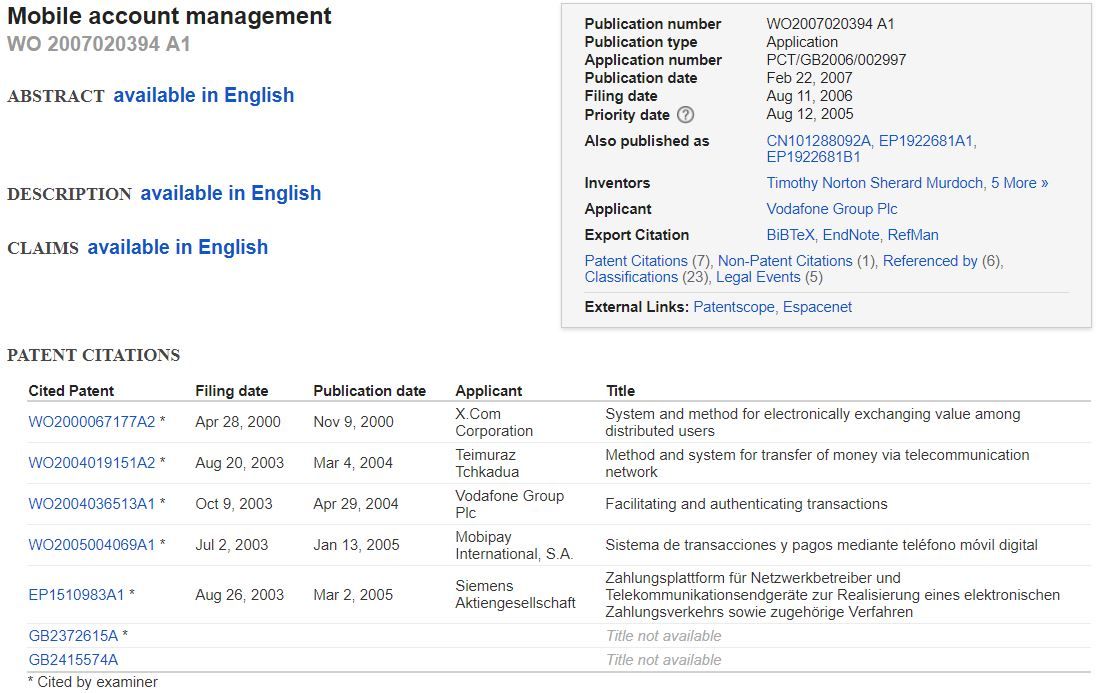

According to Waita, Vodafone filed an international patent application on August 11, 2006. The priority date on this application is August 12, 2005, which is the effective date of filing. This was filed in Great Britain.

Based on the chronology of events, this is before Ouko dropped off his “unsolicited proposal at MJ’s (Michael Joseph’s) office in April 2006”, Waita explains.

Although Waita does not say in as many words, the conclusion then is that it is impossible for them to have stolen the “idea” if they filed a year before receiving the aforesaid “unsolicited proposal” from Ouko.

It’s not that straightforward a conclusion as some experts have pointed out, normally the first document filed is the most “raw” document filed. It could be vague and contain an unrefined idea/concept as Waita already explained M-PESA as first commissioned by Vodafone, was not a mobile money transfer system and was later refined and altered.

As such, many inventors can want to alter a “raw” filing for a patent they already have because they want to include a new design or concept instead of applying for an altogether new patent as this changes the priority of the patent. This change is allowed as long as it takes place within a year.

A curious case

Safaricom’s Corporate Affairs Director further explained that even the certificate Ouko holds from Kenya Copyright Board (KECOBO) is immaterial and of no consequence.

“It is immaterial that Nyagaka obtained KECOBO’s certificate as that body only deals with copyright. The crux of his claim is that he ‘invented’ mobile money transfer but cannot support his allegations with a patent in his name. Even the certificate he holds from KECOBO is limited to ‘literary works’ meaning that he does not even have copyright to any software that would make his invention work. The claim does not meet even the most forgiving of IP law requirements that one would have to meet in order to claim ownership of a proprietary right in a product or process. Which is why the matter has not been presented to a competent legal authority for determination."

Waita contoured to explain that whereas Nyagaka’s story is for all intents and purposes an attractive tale of an enterprising Kenyan youth with a good business head on his shoulders, it is not a story that lends itself to any credibility in as far as his claim to being the inventor of M-PESA is concerned.

"There is no truth to his claims whatsoever and really the onus is on him to demonstrate beyond a written concept on airtime to cash transfer that he had an idea about the actual functionality of the product that is M-Pesa, its technological design, its process flows, its cost implications and implementation process. I would in this context urge you to be circumspect as you conclude the final part of your story and consider just how much work it took to develop M-Pesa to its current form and whether the claims made by Nyagaka match up to scrutiny. We will leave this to you and your readers as it is indeed a curious case.” concluded Waita.

Response from Safaricom

Safaricom responds to the M-PESA article

Dear Tefo,

Executive Summary :-

Thanks again for reaching out to us to seek our comments on the development of M-PESA. It gives us a useful platform to put to rest some of the misconceptions that have existed within the tech community.

I would first start by addressing the question of whether the origin M-PESA is Kenyan or British. The answer is neither, as you will see from the write up below, M-Pesa as a mobile money transfer platform is the product of years of collaborative research and innovation driven by teams in Kenya, the UK and other parts of the world. As to who owns the intellectual property rights in M-Pesa, that is also quite simple, the IP is in two forms, i.e. the trade mark and the proprietary software design and functionality. The IP in the trade mark M-PESA is jointly owned by Vodafone and Safaricom in Kenya, while Vodafone owns the trademark outside Kenya. The IP in the technology ( read patents) is owned by Vodafone.

The Details

The article “Is M-Pesa really Kenyan or British?” is not entirely inaccurate in terms of the history of the development of M-PESA to the extent of the involvement of Vodafone, DFID and others. However, the story fails to mention that the product/service for which VF was granted funding was actually a microfinance repayment solution. It was piloted in Thika, Kenya by Safaricom and Faulu Kenya. During the pilot, Safaricom realized that people would use the system to transfer money and not to repay their loans as they had the menu on their phones. At this juncture Vodafone commissioned Sagentia to re-write the software as a mobile money transfer solution. It was never launched as a microfinance product and Faulu did not come on board until 2011.

The un-replicated success of M-PESA would not have been possible had it not been for Safaricom’s management support led by Michael Joseph and his team, Safaricom heavy investment in yet the most ubiquitous mobile money transfer distribution network in the world has been immense. The banking architecture and distribution networks that support the M-Pesa functionality were developed entirely by Safaricom, however some of those business methods are unique to Kenya and cannot automatically be replicated in other markets due to different operating and regulatory dynamics in those areas.

Regarding the IP story, the following are the facts:

1. The intellectual property rights in the Vodafone Money Transfer (VMT) system which is the core technology platform running the M-PESA system belong to Vodafone. This is not to say that Vodafone was the pioneer of mobile money transfer systems because as at least two existed in the Philippines before M-PESA , e.g. GCash by Globe Telecom. However Vodafone and Safaricom were the first to develop a successful and globally recognized money transfer platform and have effectively set the standards for all other competing systems.

2. The M-PESA trademark is jointly owned by Vodafone and Safaricom in Kenya. Safaricom has no proprietary interest in similar trademarks outside Kenya/elsewhere in the world.

Regarding the claims by Nyagaka Anyona Ouko:

1. Nyagaka was one amongst many Kenyans who used airtime as a cash equivalent. By his own admission his cash transfer system was based on airtime. It did not comprise a ‘wallet’ distinct from the customer’s airtime. Whether that ‘invention’ is patentable or not is debatable. It is also noteworthy that airtime to cash conversion has existed in Kenya from the inception of the prepay voice product.

2. Nyagaka would have to demonstrate the novelty of his idea and the inventive step for it to be patentable. Even if it were deemed by KIPI to be patentable (which apparently it was not, hence his referral by KIPI to KECOBO), the patentability of his invention would not invalidate the VMT solution or mean that VMT infringed on his invention. Indeed there are other similar platforms the world over – Obopay, Fundamo, Com Viva, etc.

3. Vodafone files an international patent application on 11 August 2006. The priority date on this application is 12 August 2005, which is the effective date of filing, having previously been filed in GB on that 2005 date (before Nyagaka dropped off an unsolicited proposal at MJ’s office in April 2006). The patent application is publicly available on this link: http://patentscope.wipo.int/search/en/detail.jsf?docId=WO2007020394&recNum=1&maxRec=1&office=&prevFilter=&sortOption=&queryString=FP%3A(WO+2007020394)&tab=PCT+Biblio and is also attached.

4. It is immaterial that Nyagaka obtained KECOBO’s certificate as that body only deals with copyright. The crux of his claim is that he ‘invented’ mobile money transfer but cannot support his allegations with a Patent in his name. Even the certificate he holds from KECOBO is limited to ‘literary works’ meaning that he does not even have copyright to any software that would make his invention work. The claim does not meet even the most forgiving of IP law requirements that one would have to meet in order to claim ownership of a proprietary right in a product or process. Which is why the matter has not been presented to a competent legal authority for determination.

Whereas Nyagaka’s story is for all intents and purposes an attractive tale of an enterprising Kenyan youth with a good business head on his shoulders, it is not a story that lends itself to any credibility in as far as his claim to being the inventor of M-Pesa is concerned. There is no truth to his claims whatsoever and really the onus is on him to demonstrate beyond a written concept on airtime to cash transfer that he had an idea about the actual functionality of the product that is M-Pesa , its technological design, its process flows, its cost implications and implementation process. I would in this context urge you to be circumspect as you conclude the final part of your story and consider just how much work it took to develop M-Pesa to its current form and whether the claims made by Nyagaka match up to scrutiny. We will leave this to you and your readers as it is indeed a curious case.

VBR

Nzioka Waita

Director, Corporate Affairs